Tax 101: Taxes on Ordinary Income

How taxes on ordinary income have changed this century—and might change again in 2025. Dive into the exciting world of federal marginal income tax brackets and rates!

Published: March 13, 2024

I drafted the first iteration of this memo as the legislative director for a member of Congress over a decade ago, way back during Pres. Obama’s first term, when we were facing the expiration of the 2001 and 2003 Bush tax cuts. We punted that fight in 2010, as you might recall, and didn’t deal with it until the fiscal cliff battle in 2012—after the president had won reelection running on an explicit promise to let the tax cuts for the wealthy expire.

Since then, I’ve been updating this memo every time there’s another change to federal income taxes… which it turns out, has been kinda frequent. When Republicans hold a trifecta, they use the budget reconciliation process to slash federal income taxes (and a bunch of other taxes too) without having to face a filibuster in the Senate. But while reconciliation rules allow you to blow the budget to hell and back in the first ten years, you’re not allowed to increase deficits in the “out years” beyond the first 10-year budget window. Hence the expiration dates given to the Bush and Trump tax cuts. And when some of those tax cuts expire under Democratic administrations, there are often political calculations that lead to additional changes… and some weird outcomes.

But first things first…

What are federal income tax brackets?

Federal marginal income tax brackets reflect the rates that you pay on different sections of your taxable income.

-

Keep in mind that the income being taxed is not total (or gross) income but taxable income only. Taxable income is achieved by subtracting deductions and exemptions from gross income. Remember that deductions reduce your taxable income; credits reduce your final tax payment. (I got into more detail HERE.)

If you’re in the 22% bracket, that does not mean that you pay 22% on your entire income.

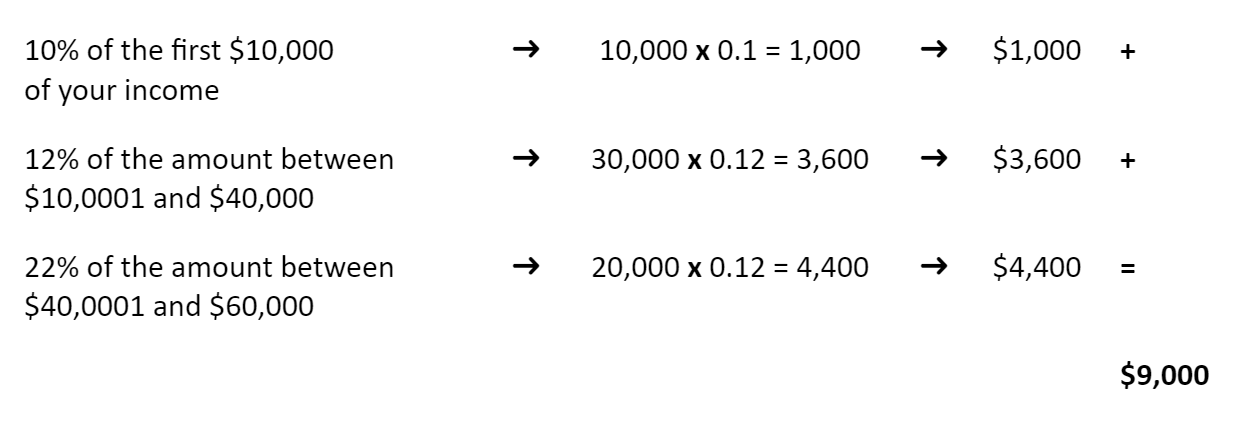

As a simplified example, let's say that you're single and you have a taxable earned income of $60,000 for the year. Your tax liability is NOT 60,000 x 0.22 (which would be $13,200).

Instead, your tax liability is determined by calculating the tax for each slice of your income and then adding the taxes together.

So, in our example (using round numbers to make it easy), it’s:

Your tax liability in our example is therefore $9,000.

(If you want to visualize it in a different way, this bucket metaphor is pretty great!)

This structure contributes to both the fairness and the progressivity of the tax code: everybody pays the exact same tax rate on the same amount of income. Nurses and NBA players each pay 10% on their first ten grand, and 12% on their next thirty grand, and so on.

But this structure also really confuses the public about how much they’re paying. Even taxpayers who’ve been paying taxes for years don’t necessarily know how the brackets work because news articles usually focus on the top tax rates. Or they know, but forget, because life is complicated and none of us get enough sleep. Financial advisers are often asked if clients should turn down a pay raise to avoid higher taxes. Conservatives exploit that confusion, so it’s worth explaining it in simple terms whenever possible.

Furthermore, because of this structure, every reduction in the rates for lower brackets also lowers the tax liability for high-income individuals, even if the top tax rates stay the same. A millionaire whose top rate returns to 39.6% will still benefit—even if it’s a small amount relative to his overall income—from lower rates on the part of his taxable income that falls in the lower brackets. (In contrast, cutting the top brackets does nothing to help those lower down the ladder.)

This question came up a lot when the Bush tax cuts were expiring. The top rate increased, but wealthy families still got some benefit from the extension of the Bush-era rates on the lower brackets.

This is part of the reason why “middle-class tax cuts” (at least insofar as they mean rate cuts on the lower brackets) still cost a lot of money: they benefit everyone. (The other reason, of course, is just that there are a LOT of middle-class taxpayers.)

So how have the brackets—and the income that falls in each section—changed over the years?

The 2001 and 2003 Bush tax cuts created a new 10% income tax bracket for the first $8,000 (single) / $16,000 (married) dollars of income. (Those filers had previously been taxed at the 15% rate). The Bush tax cuts also reduced the previous brackets from 28%, 31%, 36% and 39.6% to 25%, 28%, 33%, and 35%, respectively. Finally, the Bush tax cuts increased the amount of income allowed under each bracket, pushing more people (with higher incomes) into lower brackets than they would otherwise have been in.

(This gets really confusing really fast, so I’ve put all of changes into tables below, using letters to keep track of how each bracket changed over the years.)

-

Brackets are not referred to as “A,” “B,” “C.”. This is just a visual trick I’m deploying to compare apples to apples, or C bracket to C bracket, so that we know the 28% bracket in 1999 is the equivalent of Trump’s 22% bracket, not today’s 28% bracket. Tracking those changes is helpful for understanding why the Bush and Trump tax cuts are such big drivers of today’s deficits and why we’d be on a very different fiscal path if the Supreme Court had decided Bush v Gore the other way.

The Obama-era fiscal cliff deal retained the Bush brackets, added a new penultimate bracket at 35%, and bumped the rate for the highest bracket back up to 39.6%. (This new 35% bracket only affected a very small slice of income, but creating it allowed lawmakers to say that taxes were not going to go up for those making less than $400,000 for single filers or $450,000 for married filing jointly. I told you political promises led to weird policy outcomes sometimes!)

The 2017 Trump tax law retained the Obama-era structure of seven individual income tax brackets, but it lowered the rates for five of them and kept the rates the same for the other two—a fairly straightforward tax cut for everyone except those households with the lowest incomes (since the 10% rate didn’t change). The top marginal rate was cut from 39.6% to 37%, while the 33% bracket dropped to 32%, the 28% bracket to 24%, the 25% bracket to 22%, and the 15% bracket to 12%. (The rate for the penultimate bracket stayed at 35%, but the bracket itself changed a LOT.)

Historical brackets via Tax Foundation. Click on any table image to go the Google Doc where they all live.

In an opposite move from the Bush era tax cuts, the Trump tax cuts reduced the amount of income allowed under each bracket (relative to the Obama-era law) for the middle brackets. That meant pushing more people (with lower incomes) into higher brackets than they would have previously been in. While the Bush-era tax law had been a straightforward tax cut for the middle brackets, the Trump-era tax law was more of a mixed bag (for lots of reasons), and some tax filers with upper middle incomes found themselves in a higher bracket than they had been in previously.

For example, individuals at the high end of the Obama-28%[D] bracket (say, those making $190K) now topped out in the Trump-32%[E] bracket. Individuals at the high end of the Obama-33%[E] bracket (making $250K) were now in the Trump-35%[F] bracket.

Now, if you’re having trouble following how the Trump tax law messed with income thresholds because of the inflation-driven differences between 2016 and 2024, don’t worry, I HAVE MORE TABLES!

It’s really clear once you compare 2025 (the last year the Trump tax cuts are scheduled to be in effect) with 2026 (the first year they’re scheduled to revert back to the Obama-era rates).

An individual with $500K in taxable income in 2025 will top out at the 35% rate under the Trump rules, but if the Obama-era rules return in 2026, would only top out at the 33% bracket (owing about $1000 less in taxes if the Obama code returns—not counting tax credits, etc).

But here’s what’s really impressive. At the same time that the Trump law decreased the income threshold for the 35% bracket, it significantly increased the income threshold dividing the 35% bracket and the top bracket (37%), sheltering more income from the very wealthiest households in the lower (35% rate) bracket—a straightforward tax cut, but only for those with the highest incomes.

These are the income cut-off levels for single filers only. The distribution for married-filing-jointly filers is much less wacky, but similar in its treatment of the 33-35% brackets. Data via CBO

This is the same data as the chart above (rounded to the nearest $10K for simplicity) to show how the Trump tax law changed income thresholds for the upper middle brackets to pay for a larger cut for the very wealthiest incomes. You can see how people who would have maxed out in the 33% bracket under Obama now find themselves maxing out in the 35% bracket under Trump. Side bar: see that tiny little $2K slice for the 35% bracket that’s set to return in 2026? Weird, right? That was necessitated by the last Democratic president’s pledge to not raise taxes on those over $400K.

We don’t have to cry too many tears for the people making $500,000 a year to still marvel at how brazenly the law dings them to help the tycoon class. It’s just a remarkably straightforward example of making people lower down the income scale (including the merely wealthy) pay for tax cuts for the very wealthy.

These Trump-era changes are set to expire at the end of 2025. Biden’s FY 2025 budget (released March 11, 2024) promises to “restore the top marginal tax rate to 39.6 percent for single filers making over $400,000 a year and married couples making more than $450,000 per year.”

If enacted, that would, in essence, cleave in two parts the income range currently tied to the 35% rate, with the income under the $400k/$450K threshold presumably topping out at 35% while income over that threshold would be taxed at the restored 39.6% rate.

One additional note: The Trump tax law also made one other big change to the amount of income in each threshold: changing the inflation-adjustment calculation to “Chained CPI,” which (in normal years, anyway) leads to a smaller increase than the previous inflation adjustment. While the bracket changes are set to expire at the end of 2025, the switch to chained CPI was made on a permanent basis.