The Dumbest Tax Editorial

This week, the Wall Street Journal editorial board, that comforter of the comfortable and afflicter of the afflicted, published an attack on Biden’s proposal to equalize the federal tax rates levied on income gained through investments and income earned through working. Equalizing rates is one part of his strategy to “tax wealth like work” so that wealthy investors aren’t given a better deal than hardworking Americans. Surprise surprise, the editorial was chock full of inaccuracies, so I got out my proverbial red pen and fixed it for ‘em.

The Dumbest Tax Increase Editorial

Biden’s capital-gains rate of 43.4% would reduce raise $324 billion in federal revenue.

By The Editorial Board, Wall Street Journal + your tax fairness friend Sarah

Published: April 25, 2021. Corrected: April 30, 2021.

If you need more evidence that ideology more than common sense is driving the Biden presidency, look no further than its trial balloon to raise the top tax rate on capital gains to 43.4% for the wealthiest Americans. It’s a smart the dumbest way to raise taxes for many reasons, not least because it will cost the government revenue raise $324 billion over 10 years while simultaneously eliminating multiple market-distorting provisions in the current code. But we’ll get to that later.

First, let’s clarify what’s under consideration. The Biden plan would restore the top marginal tax rate on ordinary income to the pre-Trump rate of 39.6%. It would then equalize the top rate paid on investment income to the rate paid on income from working, so that a playboy heir sitting by the pool during COVID would finally pay the same rate on his investment income as an ER doctor working 24-hour shifts through COVID pays on his salary.

So how do we get to 43.4%? The ACA created a 3.8% net investment income tax (NIIT) on capital gains made by high-income earners. If 3.8% sounds familiar, that’s because it’s equivalent to the Medicare payroll tax rate paid by self-employed high-income earners on their salaries and wages. Other than the NIIT, there is no payroll tax equivalent for capital gains income.

Keep payroll taxes in mind when we get to the bogeyman of “double taxation.” And remember, no Social Security taxes are collected on investment income at all.

The premise behind the tax increase is that a preferential tax rate for long-term capital gains is an unjustified loophole. (Gains on assets held for less than a year are taxed at the individual income rate.) Yet that preferential rate has persisted for decades, through Democratic and Republican administrations.

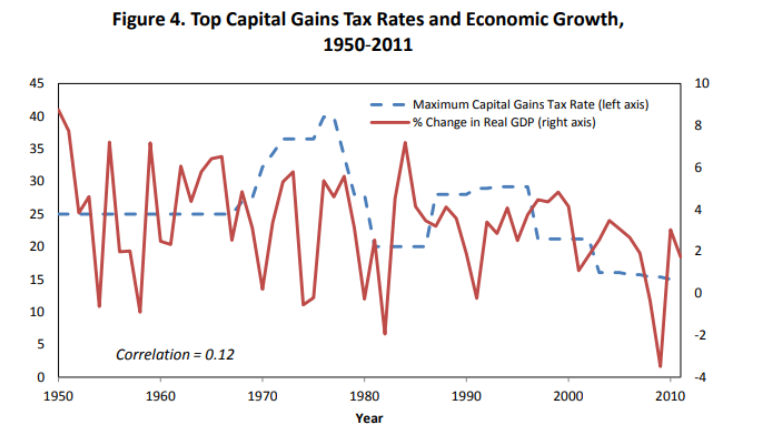

It’s absolutely true that when the top marginal tax rate on ordinary income in the U.S. was 77% and 84% and 92%, the capital gains rate was lower than that. You got us! The current top rate is 23.8%, which includes a 3.8% ObamaCare surcharge. Even in the economically irrational 1970s the top capital-gains rate never broke 40%, as the nearby chart shows. This is a tad disingenuous in that the capital gains rate has often been higher—and even quite a bit higher—than the rate in place today.

***

There are no good economic and fairness reasons for the preferential rate that withstand scrutiny. First, under current tax rules, all gains from investments are fully taxed, but all losses are not fully deductible. Losses can offset gains in any given year, but losses that exceed gains can only be offset against personal income up to $3,000. The preferential rate far over-compensates for this asymmetry.

Let’s clear something up. Capital losses can fully offset capital gains, and unused losses can be carried over to offset gains in future years. Remember that, because it’s going to be important when we look at Jeff Bezos’s 0% federal income tax rate in the years that his Amazon holdings grew by billions of dollars.

But kudos, I guess, to the Wall Street Journal editorial board for not justifying a capital gains rate that is nearly half the top tax rate for earned income by arguing, as many anti-tax proponents do, that the preferential rate is needed to reward the risk of investing—as though investing were riskier than, say, logging, fighting fires, treating COVID patients, policing high-crime neighborhoods, protecting students during active-shooter attacks, or building skyscrapers.

If you’re a firefighting supervisor, the 9th deadliest job in America, half of your $88,000 taxable income in 2021 is taxed at 22% (not counting payroll taxes of 7.65%). But if you make a multi-million-dollar income through capital gains, your income is taxed at just 20% (with a just 3.8% surtax). Hats off to the anti-tax crowd who can boldly proclaim that the lower rate is justified by the risk involved.

Second, gains in asset values aren’t adjusted for inflation, so investors who hold assets for an extended period pay taxes on increases that are partly illusory. Other parts of the tax code, including the income-tax brackets, are indexed for inflation, but not capital gains that arguably need it the most since assets are often held for decades. I, for one, am pleased to see the Wall Street Journal argue in favor of tax preferences, such as expanded refundability for low-income workers, in recognition of the reality that the minimum wage has never been tied to inflation.

But if you’re curious about this issue, the non-partisan Tax Policy Center wants you to know that yes, “it is true that inflation causes part of almost any nominal capital gain. But inflation actually affects the returns on currently taxed assets (interest, dividends, rents, and royalties) more than it affects capital gains, which are taxed when an asset is sold.”

Similarly, leading tax economist Leonard Burman — who helped draft the 1986 tax reform and worked over 10 years for the Congressional Budget Office — testified before the House and Senate tax-writing committees in 2012 that inflation “is an argument for indexing the whole tax system (Shuldiner 1993), not a preference targeted at capital gains. In fact, the benefit of deferral may offset part or all of the inflation tax. (Burman 1999) This isn't true for assets that pay annual income such as bonds and rental properties. So if there is an argument for selective inflation relief, it would apply with most force to income other than capital gains.”

Third, a capital-gains tax is a second tax on corporate income. A neutral revenue code would tax all income only once. But the U.S. also taxes business profits when they are earned, and President Biden wants to raise that tax rate by a third (to 28% from 21%). When a business distributes after-tax income in dividends, or an investor sells the shares that have risen in value due to higher earnings, the income is taxed a second time.

No less a progressive than Democratic Rep. Jerry Nadler recently deplored the unfairness of “double taxation” regarding and state and local tax deduction, though he probably had no idea he was stating a principle that really applies to corporate income and capital gains.

Ah yes, double taxation. So we’re just gonna pretend that payroll taxes don’t exist? Or federal excise taxes? Neither kind of taxes is deductible from individual income taxes (both are deductible from business taxes, so no double taxation there). And both kinds are regressive, in that they take a much bigger bite out of low- and middle-income families. Some, such as the gas tax, can be particularly burdensome for rural Americans. This year, top Republicans in Congress have proposed to levy new excise taxes in order to avoid raising revenue from the ultra-wealthy, which makes concerns about double taxation a little absurd. But set all of that aside for a moment and consider the argument on its merits.

Again, the non-partisan Tax Policy Center notes: “The double-taxation argument goes only so far. Capital gains from the sale of stock are only about half of all capital gains. And even when a gain arises from the sale of corporate stock, corporate profits can often escape full taxation through business tax preferences.”

When dozens of Fortune 500 companies are paying zero in federal income taxes while raking in profits hand over fist, it’s downright impressive to argue double taxation with a straight face.

But while double taxation of capital gains can be a farce, never-taxation is very real. How does a multi-billionaire like Jeff Bezos get away with paying no federal income taxes in multiple years? Part of it is the deductibility of investment losses that the WSJ decried above as woefully insufficient.

In its bombshell report on just how little federal income taxes American billionaires pay, ProPublica found:

Consider Bezos’ 2007, one of the years he paid zero in federal income taxes. Amazon’s stock more than doubled. Bezos’ fortune leapt $3.8 billion, according to Forbes, whose wealth estimates are widely cited. How did a person enjoying that sort of wealth explosion end up paying no income tax?

In that year, Bezos, who filed his taxes jointly with his then-wife, MacKenzie Scott, reported a paltry (for him) $46 million in income, largely from interest and dividend payments on outside investments. He was able to offset every penny he earned with losses from side investments and various deductions, like interest expenses on debts and the vague catchall category of ‘other expenses.’

In 2011, a year in which his wealth held roughly steady at $18 billion, Bezos filed a tax return reporting he lost money — his income that year was more than offset by investment losses. What’s more, because, according to the tax law, he made so little, he even claimed and received a $4,000 tax credit for his children.

But even more importantly, Bezos and his cohorts in tax avoidance never have to pay taxes on their investment income until they sell, and if they need cash, they just borrow against their assets… and then they deduct the interest payments. They have access to all the cash they need, without ever having to pay taxes on it. Pretty sweet.

And if Bezos holds onto his $200 billion in Amazon stock and never sells? Then he’ll go his entire life without ever paying federal taxes on it. And thanks to the “stepped-up basis” loophole, his adult heirs will get handed $200 billion in stock that they can sell the same day without paying a single cent of federal taxes on. More on that later.

A-mazing.

But it gets better.

The most important reason to tax capital investment at low rates is to encourage saving and investment. Consumption—buying a car or yacht—faces a sales tax but not a federal tax—except for all of those examples where consumption faces a federal excise tax. Has no one at WSJ ever bought gas?

But if If someone saves income and invests in the family business or in stock, he is smacked with another round of taxed, but only on his gains. Let’s say your after-tax income is $100, which you invest in an asset that increases in value by $200. When you sell, you are not then subsequently taxed on the full $300, but rather once on the first $100 and once on the $200 gain.

Tax something more and you get less of it. This can be true, which is one reason we tax cigarettes and tanning, but in actual real-world practice, it turns out that it’s a lot more complicated when it comes to investment—in part because the marginal differences in behavior are: smoke or don’t smoke, tan or don’t tan, make money or… don’t make money. Tax capital income more, and you get less investment, which means less investment to improve worker productivity and thus smaller income gains over time.

As a former U.S. President once put it: “The tax on capital gains directly affects investment decisions, the mobility and flow of risk capital from static to more dynamic situations, the ease or difficulty experienced by new ventures in obtaining capital, and thereby the strength and potential for growth of the economy.”

That wasn’t Ronald Reagan. It was John F. Kennedy, whose chief economic adviser was liberal Keynesian Walter Heller. A Democrat who said that today would be excommunicated, but it’s nonetheless true because it’s false.

We’ve learned a lot since the 1960s, which is why we no longer put lead in our gasoline and asbestos in our homes. With all due respect to JFK, decades of actual tax policy and economic data prove, well, he was wrong. But don’t take my word for it. Here’s the data.

Tax Policy Center: “Many factors determine growth, but the tax rate on capital gains does not appear to be a major factor.”

Burman testimony: “The heated rhetoric notwithstanding, there is no obvious relationship between tax rates on capital gains and economic growth. Figure 4 shows top tax rates on long-term capital gains and real economic growth (measured as the percentage change in real GDP) from 1950 to 2011. If low capital gains tax rates catalyzed economic growth, we’d expect to see a negative relationship – high gains rates, low growth, and vice versa – but there is no apparent relationship between the two time series. The correlation is 0.12, the opposite sign from what capital gains tax cut advocates would expect, and not statistically different from zero. Although not shown, I’ve tried lags up to five years and using moving averages, but there is never a larger or statistically significant relationship.”

In theory, higher taxes on investments like stocks should make them less appealing. But the outlook for economic growth and corporate profits is often a much bigger factor in the decision to buy, sell or hold on to a stock. …

“Markets can grow, and grow above trend, even if you’re taking the capital gains tax rate up,” said Lori Calvasina, head of U.S. equity strategy at RBC Capital Markets in New York. … Ms. Calvasina’s team looked at what happens to the stock market when the capital gains tax rises. When the rate increased in past years, the team found, the S&P 500 index rose roughly 11 percent.

Proposed increases to the capital gains tax can cause momentary wobbles as investors try to lock in the appreciation on current investments, but the market usually regains its footing and shares climb higher.

“Any potential equity selling will be short lived and reversed in subsequent quarters,” Goldman Sachs analysts wrote late last year about the prospect of a capital-gains tax increase under Democratic control in Washington.

In 2013, when the tax rose to the current 23.8 percent, from 15 percent, on Americans with the highest incomes, the S&P 500 climbed nearly 30 percent. It was the best year for stocks in the last two decades. And after the top rate rose to 28 percent, from 20 percent, at the end of 1986, the market continued to roar higher, by nearly 40 percent through most of 1987.

If you’re wondering why markets aren’t linked to the capital gains rate, Warren Buffett has the answer:

Suppose that an investor you admire and trust comes to you with an investment idea. “This is a good one,” he says enthusiastically. “I’m in it, and I think you should be, too.” Would your reply possibly be this? “Well, it all depends on what my tax rate will be on the gain you’re saying we’re going to make. If the taxes are too high, I would rather leave the money in my savings account, earning a quarter of 1 percent.” Only in Grover Norquist’s imagination does such a response exist. …

[M]aybe you’ll run into someone with a terrific investment idea who won’t go forward with it because of the tax he would owe when it succeeds. Send him my way. Let me unburden him.

The last resort of progressives is that raising the capital-gains tax will raise revenue. They are wrong right on that too. As former Federal Reserve Governor Larry Lindsey explains nearby, a 43.4% federal rate will cost the government money, unless you fix the “stepped-up basis” loophole, which is exactly what Biden is proposing we do. The Congressional Budget Office says the revenue-maximizing rate for capital gains without fixing that loophole is about 28%. Other economists say it’s lower, and many think the ideal rate is zero. No one outside the fever swamps thinks it is more than 40%, much less the 55% or more that would apply in high-tax states if the Biden a strawman proposal we just fabricated that is not what Biden is proposing becomes law.

The history of capital gains taxations bears this out. Selling an asset is usually a discretionary decision, so investors can decide when to realize a gain or loss. As rates rise, Americans tend to hold on to their assets longer, reducing realizations. CBO has found that for each 1% increase in the capital-gains rate, there is a 1.2% reduction in realizations. Raise the tax as much as Mr. Biden wants, and realizations will fall significantly. The higher rate will cost the government revenue.

Again, here the WSJ is just willfully ignoring that Biden is not only proposing to equalize the rate, but also to close that market-distorting loophole I mentioned above known as “stepped-up basis.” (A wealthy heir’s “basis,” aka purchase price, gets artificially stepped up to whatever the asset was worth on the day he inherited it, instantly wiping out millions or billions of dollars in gain.) This is how hundreds of billions of dollars in Amazon stock will go completely untaxed when Jeff Bezos dies, consolidating more and more gargantuan fortunes in family dynasties.

This absurd-on-its-face loophole treats capital gains made from selling an asset one month before you die as taxable and the gains made from your heirs selling the same asset at the same price one month after you die as tax-free (!). Guess what happens when the tax code arbitrarily picks winners and losers based on whether or not they can afford to hold onto an asset until death? The market reacts.

Instead of making smart investment decisions based on the best use of capital, the wealthiest who are nearing the end of their natural lives simply hold on to ensure that they don’t have to pay any tax on their gains at all. In the Warren Buffett example above, the difference is between taking home a little more or a little less in pure profit based on the tax rate. As he says, he’s never going to pass up the chance to make money just because he’ll keep slightly less of it. But that’s not the choice under stepped-up basis. That choice is pay taxes now, or wait a few years and cash out billions of dollars in assets without paying any taxes at all.

And here the WSJ gets something right: that loophole is so market-distorting that leaving it in place is literally the difference between raising $324 billion and losing $33 billion. That’s one hell of a distortion!

But that’s not all. The low rate on capital gains itself distorts the market, driving capital to seek arbitrage opportunities instead of productive investments.

Here’s the kicker, again from the Tax Policy Center:

Low tax rates on capital gains contribute to many tax shelters that undermine economic efficiency and growth. These shelters employ sophisticated financial techniques to convert ordinary income (such as wages and salaries) to capital gains. For top-bracket taxpayers, tax sheltering can save up to 17 cents per dollar of income sheltered. The resources that go into designing, implementing, and managing tax shelters could otherwise be used for productive purposes.

Finally, the low rate on capital gains complicates the tax system. A significant portion of tax law and regulations is devoted to policing the boundary between lightly taxed returns on capital assets and fully taxed ordinary income.

And from Leonard Burman, 2021: “A whole industry of tax planners devotes their considerable skills to converting high-taxed ordinary income into lightly taxed, or untaxed, capital gains. This saves high-income people billions of dollars in taxes and represents a giant waste of economic resources. Many of these schemes make no economic sense – but for the tax advantages.”

(Side bar, that whole Burman piece is great. Go read it!)

Fortunately, Biden is proposing that we both equalize the rate and close the loopholes, leading to the most efficient and effective use of capital for investment and economic growth.

And finally, while the WSJ doesn’t touch on this piece, let me: raising the capital gains rate and closing the stepped-up basis loophole for people with incomes over $1 million won’t affect middle class taxpayers—by definition.

But it also won’t affect pension funds, nonprofits, retirement plans or 401(k)s, college endowments, or life insurance companies. Why? Because they aren’t subject to capital gains taxes. (Also, remember that when you’re retired and withdrawing from your 401(k) or traditional IRA, you’re paying taxes at ordinary income rates.)

And the administration has already proposed special carve-outs for family-owned farms and small businesses. This is about making sure that Bezos, Elon Musk, George Soros, Warren Buffett, and yes, even Rupert Murdoch and the fine folks at the WSJ, pay some damn taxes at a rate like the rest of us.

***

So why write an editorial that misstates core facts and obfuscates others to pretend the opposite of what the data make clear raise a tax rate that would reduce investment, reduce wage growth and reduce revenue for the government? Temporary economic insanity is one possible explanation.

Mr. Lindsey suggests another: punishment for its own sake. Without a rational basis for the tax increase, this sounds right. This is what happens when you turn your economic policy over to Bernie Sanders and Elizabeth Warren. Envy is in the political saddle, and Joe Biden is going along for the ride.